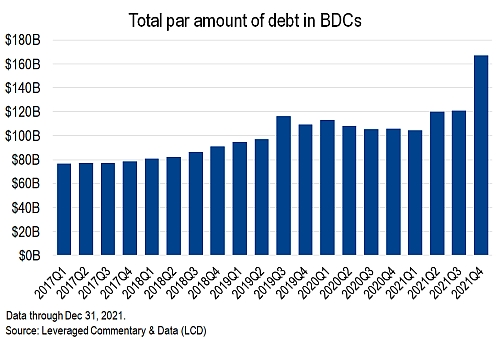

Growing use of private credit in leveraged finance, at the expense of syndicated loans, is increasingly apparent in the investment portfolios of business development companies, LCD data show. The trend toward non-broadly syndicated loans versus broadly syndicated loans in BDCs was illustrated both by issuer count and par amount as of the fourth quarter of 2021.

.jpg)

.jpg)

The activity in the final quarter of 2021 confirms that BDCs have shaken off the slowdown in volume beginning in 2020, brought on by the Covid-19 pandemic.

In fact, LCD data show that in the fourth quarter of 2021, growth of loans in BDCs reached an all-time high, both by number of issuers and volume. In the final months of last year, many BDCs had reported record originations. According to market sources, activity levels have since slowed, as volatility keeps dealmaking at bay and borrowers react to rising interest rates.

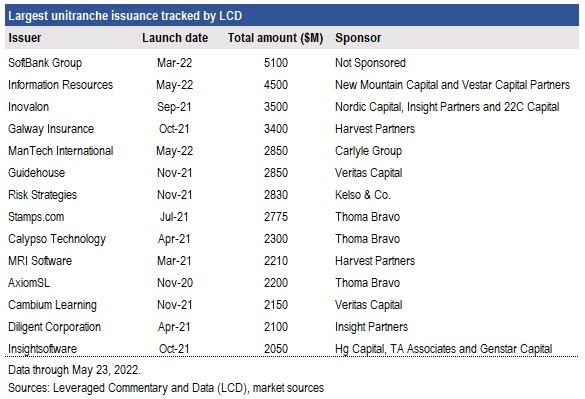

In recent quarters, private credit providers have shown an appetite to finance ever-larger loans for buyouts. This could be one explanation for non-BSL loans taking on a bigger share of BDC investment portfolio holdings than in the past, as BDCs help absorb these enormous financings.

In fact, in recent months, some of the largest unitranche loans ever have come to market. The unitranche loan, the core product of the private debt market, blends senior and junior debt into a single tranche.

The increase in non-BSL loans in the fourth quarter is the culmination, so far, of a change in recent years that coincided with the growth of private credit.

In 2016, the share of non-BSL and BSL assets in BDC portfolios (based on par amount) was split roughly evenly, according to LCD data.

According to the most recent data available from Preqin, private credit assets under management totaled $1.23 trillion as of September 2021. This compares to $573 billion as of December 2016.

LCD tracks the portfolio holdings of 72 publicly traded and private BDCs.

Follow Us

© 2026 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means-graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems-without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as investment advice, a past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.