For years, private credit providers have honed their messaging to explain why their loans are superior to financing in the broadly syndicated market. Now they are adjusting their pitch to explain why private debt may be better than another longstanding pillar of leveraged finance — high yield bonds.

There are signs this effort may have worked in recent months.

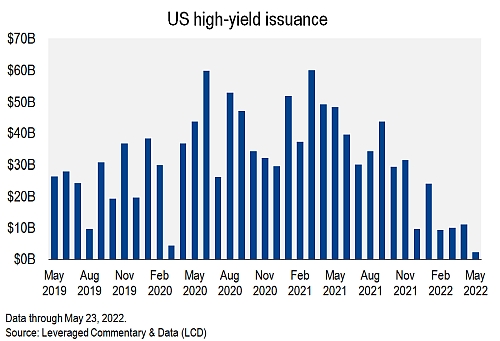

The volume of high-yield bond issuance has plunged this year in the face of market volatility. That’s not unusual when equity markets swing wildly. But private credit providers, still flush with cash, have swooped in, underwriting transactions that may have been done in the traditional high-yield bond market in the past.

For example, investors heard last week that financing for the proposed buyout of Nielsen Holdings will now include a $2.15 billion second-lien term loan facility to replace an unsecured bridge facility of the same size that was part of the original commitment. Private credit providers have stepped up for the unsecured part of the financing. Lenders are Ares Management Corp., Carlyle Global Credit, PSP Investments Credit USA, Fortress Credit, BC Partners, Grosvenor Capital Management, Oaktree Capital Management, GoldenTree Asset Management, Stone Point Credit, and T. Rowe Price Associates.

The first-lien financing for Nielsen is unchanged: a $6.35 billion secured term loan, a $650 million secured revolver, and a $2 billion secured bridge facility. Elliott Investment Management and Brookfield Business Partners are acquiring Nielsen in a deal valued at around $16 billion. The transaction is expected to close in the second half of 2022.

Nielsen is a seasoned high-yield issuer. But for this deal, it looks as if Nielsen will do nothing to boost the paltry high-yield volume so far in 2022. In fact, May has been one of the leanest high-yield months on record, LCD data show.

Of course, any potential new bond issuance would have had to take these secondary trading levels into account.

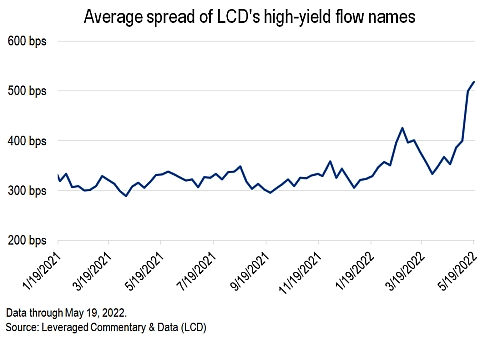

It would be more expensive to issue bonds today versus even just a few months ago. High-yield paper has dropped precipitously in recent months as investor demand has evaporated alongside rising interest rates: Nielsen 4.75% senior unsecured notes due July 15, 2031, traded on May 20 at 91.375, yielding 5.99%. For reference, the paper at year-end 2021 traded at 98.75, yielding 4.92%.

Private credit has held up better than other fixed-income asset classes. Intense competition from lenders willing to provide financing has kept spreads from increasing significantly, market sources say, but there is little actual data to back this up.

Chasing market share

There are indications that other recent issuers may have forgone high-yield bonds in lieu of private loans. It’s clear that some would-be syndicated loan borrowers have done the same. In fact, LCD data suggest that private credit has been taking a toll on the market share of leveraged loans.

“Private credit is here to stay. They’re taking advantage of ... dislocation in the high yield bond market [to] take down paper in either the leveraged loan or the unsecured bond format and ... relieve banks of some of that risk,” said Christopher Blum, head of leveraged finance at BNP Paribas.

“We’ll continue to need to compete with the private credit world. Traditionally, that paper was priced much wider than either the high yield bonds or the leveraged loans, depending on where you sit in the capital structure. When you have dislocation in the market as we’re seeing now, that obviously gives opportunity,” said Blum.

The arguments in favor of private credit over syndicated loans are, by now, well known: It’s far easier to work with just a handful of lenders, or a single lender, than with dozens or more in the case of a syndicated transaction. This is especially true in the case of a workout. A single lender group avoids the issue of various lender groups that may have competing interests.

In private credit, lenders agree to provide loans at prescribed levels and terms. This is particularly useful when markets are volatile, as they have been in recent months. Private credit’s core product, the unitranche loan, wraps senior and junior capital into a single tranche.

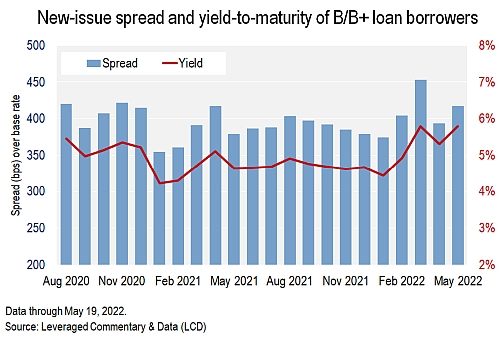

On the other hand, the syndicated loan market has typically been able to offer better pricing for borrowers. But recent market gyrations may have undercut that advantage. Indeed, the average new-issue yield-to-maturity on term loan Bs issued to borrowers rated B/B+ widened to 5.79% in March, from 4.43% in January, while the corresponding nominal spread rose to Sofr+453, from Sofr+374, respectively. The current reading for May stands at 5.8% yield/Sofr+418 spread.

For lenders, private loans are appealing because they have generally retained covenants. In contrast, the vast majority of syndicated loans are covenant-lite.

However, in a competitive market, pressure has intensified on private debt lenders to relax terms.

“When we think about market share it isn’t just against bank loans. It would be out of all the leveraged capital markets,” said Marc Lipschultz, co-chief investment officer of Owl Rock Advisors, on the sidelines of Blue Owl’s investor conference on May 20.

“It’s certainly true that our solutions meet the same need that high yield solutions could meet. When I think about the investor opportunity, high yield is an even easier and more direct conversation,” Lipschultz added.

Compared to private credit, high yield bonds generally have weaker indentures and fewer limitations that could protect lenders, Lipschultz said. Returns on the fixed-rate high yield bond asset class have historically lagged the 10-15% gross returns on floating-rate private loans that Owl Rock expects. What’s more, bonds are more junior in the capital structure than the senior loans provided in private credit, Lipschultz said.

But the performance of high yield bonds this year has made the case for private credit easier. The asset class has lost nearly 11% in 2022 through May 20, according to the S&P U.S. High Yield Corporate Bond Index.

In a testament to private debt’s popularity, in recent months, private credit providers have increasingly taken down larger deals that in the past would have been done in the syndicated loan market.

Moreover, several significant leveraged buyouts are teed up as private credit transactions. These include Anaplan, SailPoint Technologies, Kaseya’s acquisition of Datto, Information Resources Inc., Tivity Health, and ManTech International Corp.

In keeping with this trend, Latham & Watkins said in a recent report that deal sizes would continue to increase going forward. The law firm also expects lending terms available in the private credit and syndicated loan markets to continue to converge. This year, the firm expects that direct lending funds will likely go deeper in the capital structure, to the junior level, through products such as mezzanine debt, PIK or preferred equity.

“Private credit now appears on the second lien, preferred equity, and/or PIK on most syndicated deals,” Latham & Watkins said in the recent report, entitled Private Capital Insights.

“As both fund sizes and the scale of lending keep rising, we will continue to see direct lending deals taking a growing market share, competing for first and second lien structures, and often getting exclusive visibility of unitranche opportunities. As competition intensifies and the market continues to grow, we will likely see direct lenders taking on more risk on large deals, either as part of a club with other funds or co-investors or with the intent to effectively syndicate deals themselves,” the report said.

Private credit has grown significantly in recent years. According to the most recent data available from Preqin, private credit assets under management totaled $1.23 trillion as of September 2021. This compares to $573 billion as of December 2016.

Owl Rock’s Lipschultz said there’s no doubt that direct lending will continue to gain market share within leveraged finance.

“As much as people like to articulate the story of ‘it’s the banks vs. the direct lenders,’ ‘it’s the public markets vs. the private markets,’ and who’s going to win — this is a big market. There’s room for all these solutions … It’s not a ‘we win, they lose.’ It’s not one or the other. It’s going to take all these markets to meet the growing needs of U.S. businesses, and businesses around the world,” Lipschultz said.

Follow Us

© 2026 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means-graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems-without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as investment advice, a past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.